Michael Ballanger of GGM Advisory Inc. takes a look at current trends in the gold and uranium market, and shares a couple stocks in his portfolio.

For most of 2023, and in fact, since January 2020, when I first launched the GGMA Advisory service, I have been exalting the wonders of gold ownership for a myriad of reasons that date back to the 2008 GFC. Without reciting those reasons, you all know them. Whether they be geopolitical strife, profligate government spending, or banking shenanigans, if I lined them all up in 2005 and asked you to put a dollar value for gold, you would give me a number north of $5,000 per ounce. Yet, despite the vilest of debasement campaigns in the history of modern civilization, the U.S. dollar defied all logic and analysis and steadfastly refused to break out through the ceiling established back in 2011 after the U.S. government gave a blank cheque to the international banking cartel and flooded the world with greenbacks.

This week marks a watershed for me in many respects.

Gold

It validates what I have been writing about for most of my career: that gold is money and that everything else is indeed debt. Gold is the money of kings, and debt is the money of slaves. If one follows that mantra, then cash, stocks, bonds, crypto, and virtually every other form of financial asset is merely a proxy for debt and completely vulnerable to counter-party risk. For those like-minded souls who have striven all their lives for freedom from the shackles of societal pressure and government oppression, the only clear path to financial freedom has always been through the ownership of gold.

I wrote several months ago, as gold wallowed in the maddening, bullion bank-orchestrated trading range between$1,800 and $2,000, that 2024 would be the year that gold finally broke free. I urged overweight positions not in crypto or lithium or uranium or any of the “flaveur du jour” narratives that would be advanced by the legions of podcasting and you-tubing “influencers” where “talking up one’s book” (pumping stock positions one holds) has become an art form rather than the frowned-upon dalliances of the celebrity fund managers. I suggested for most of the last six months that we were approaching escape velocity for gold bullion while praying for (rather than predicting) that the gold miners would finally get the memo.

As thousands of PDAC attendees departed the hallowed halls of the Toronto Metro Convention Centre last Wednesday, leaving a trail of broken dreams and discarded presentation brochures on the littered floors, it was the uranium crowd that came away most disheartened because when the bookings were confirmed back in Q3 2023, it appeared that uranium was going to be the favored son of the convention. Prices had rocketed from $50/lb. during last year’s PDAC to a high of $105/lb. in the weeks leading up to the conference and judging from the number of uranium penny stocks exhibiting at the convention, they most certainly expected an amplified celebration of capitalism by the time the doors closed.

However, the main theme began with copper taking the limelight in the first few sessions, but by Wednesday, it was the mind-numbing explosion in gold prices that captured the fancies of the investor crowd. While I stuck to my insistence to not attend PDAC (since 2016), colleagues attending were making the tongue-in-cheek remark that “I guess there will be a ton of name changes from “lithium” to “gold” coming up!” I might add that the wannabes that pivoted from lithium to uranium in 2023 are now going to be pivoting once again back to gold, where they began as a listed shell five years ago. Such is life in the world of the junior resource sector.

I have been telling my subscribers to ignore all of the sensationalist grandstanding from all of the usual rockstar gurus that have been called for “$100 silver!” and “$300 yellowcake!” while keeping all eyes focused on the one instrument that is widely followed by the algobots that dominates the global financial markets these days which is the SPDR Gold Shares ETF (GLD:US) that actually tracks not the gold shares but rather the bullion price in what was originally supposed to be a 10:1 ratio. The non-human bid-hunters that roam the cyber world of stock trading with mountain upon mountain of central bank-and-government-created liquidity focus not upon the Comex price or the London fixes or even spot gold in New York or Shanghai; they focus on the GLD:US.

Whatever they can get their tentacles around is what they trade, and that is why the August 2020 peak at $194.45 was for me and my subscribers, the only number that counted in terms of the breakout. I wrote of the need for a “2-day close above $194.45” in order to avoid the possibility of an intraday whipsaw, and that is exactly what occurred last Monday and Tuesday as the GLD:US went out at $196.05 on Monday and then refused to look behind.

As the champagne flutes clinked and the golden pompoms were dusted off, there were some concerns that still demanded caution. The silver price still refuses to take the leadership role that precious metals bull markets demand. While up on the week, it is the GTSR (gold-to-silver-ratio) at nearly 90 is reminiscent of the post-pandemic period, where gold exploded out of the gate in response to those egregious stimulus programs launched by the Fed and the U.S. Treasury but trailed miserably by a flaccid silver response.

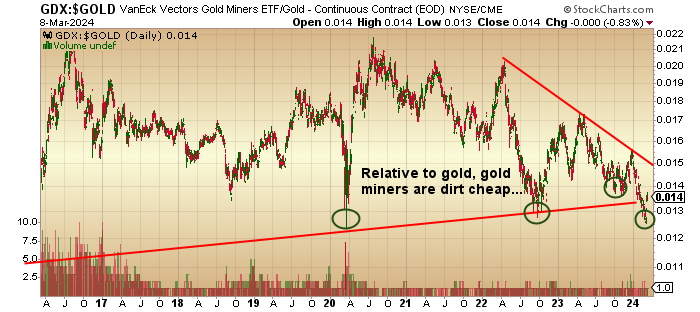

Also failing to grasp the moment were the gold miners led by the VanEck Senior Gold Miners ETF (GDX:US) whose weekly advance was impressive but still miserable relative to the gold price, as shown in this chart.

The quasi-experts that are quoted day-in and day-out on Instagram, X, and YouTube, all point to the poor management history of the global gold miners as justification for underperformance. They cite “rising input costs” or “poorly-timed acquisitions” or “too many upper management bodies” while tsk-tsking and wagging fingers disdainfully, but that argument hits the wall when one realizes that algobots that control today’s stock exchanges do not read income statements or balance sheets. They only know volume and price, and it is the interplay

between volume and price that determines “flow,” and for these AI-driven machines, that is all that counts. So, because the entire gold mining sector could be bought by a fraction of the market cap of NVidia, there is insufficient liquidity in the miners to attract even the slightest portion of the passive investment flows that automatically move into the MAG SEVEN names every month with unyielding consistency.

The other problem with this rally is that the commercial traders led by the Bullion Banks took full advantage of the breakout to lay out 48,440 new shorts, which was the largest weekly increase in the aggregate short interest in months. Mind you, the COT week ended on Tuesday, March 5, with gold going out at $2,141,90, which means that those sales were offside $44.30 per ounce by the weekly closing price.

The aggregate short interest of 206,792 is not particularly large, as I have seen that number increase to over 300,000 at other major tops. Furthermore, the price can and probably will continue to rise along with the Commercial short position until it exceeds 300,000, after which history would advise that one gets more defensive.

Newmont Corp.

The most important point in this analysis is that the algobots are now going to be forced to maintain a “Buy all dips” execution strategy rather than the “Sell all rallies,” one that they have been practicing for what seems like ages. Importantly, that pertains to gold bullion, but the real opportunity here lies in the gold miners whose value relative to the price of gold can only be deemed as “absurd.” I offer as an example the shares of Newmont Corp. (NEM:NYSE), the world’s largest gold producer and the worst-acting of the lot going into the end of February.

Newmont has made some aggressive acquisitions in recent years, obviously into what they viewed as depressed prices, scooping up Australian gold miner Newcrest Mining for $15 billion while adding roughly 15 million new ounces of gold to its portfolio. Seen as an “overpayment” by many as recently as a month ago, it may just turn out to have been a brilliant “underpayment” if the price of gold moves to $2,300-2,500 before the end of 2024. Price action always dictates the appropriate narrative until that same price action suddenly shifts, and foolhardiness turns to genius.

I learned many years ago to “Never confuse bull markets with brains,” and in keeping with the unjustified pillaging of Newmont, “Never confuse bear markets with buffoonery,” and that is exactly what the quasi-experts were doing in a gang-attack style of pile-on, bottom-of-the-market capitulation that is so typical of today’s social media bullying and narrative-chasing.

This chart (note the date) was posted the day after a notable gold “guru” (often seen sporting an oversized black cowboy hat) posted several totally vitriolic and emotional tweets referring to Newmont as an “overpriced piece of $#$%” and vowing to sell his position and never buy it back.

I posted the chart as a “contrarian buy” because I could not see how the news could get any worse and not because I was in possession of clairvoyant powers and knew that gold would break out a week later.

The NYSE ARCA GOLD BUGS INDEX (HUI:US) closing at 228 is still ridiculously undervalued when you consider that it saw its last major peak back in 2020 at 370 when gold was still under $2,100.

Getchell Gold

Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB)

Following behind in wonderful fashion, the junior gold developers are going to be rerated higher after suffering abandonment for the better part of forty-three months.

Top-ranked Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB) finally clawed its way back to $.20 and now that it was able to secure the final installment of its Fondaway Canyon acquisition from 2020, it now is 100% owner of 2,059,900 ounces of gold in the premier gold mining jurisdiction in the U.S. (Nevada) and intend to proceed to expand the resource to Tier Two status with drill programs later in the season.

I honestly cannot recall the last time that the RSI for the GLD:US moved into the ’80s, but in glancing at the 5-year chart, it turns out that it was August 2020 which marked the top of the post-pandemic rally created by the money-printing orgy that preceded it.

All momentum indicators that I use are now in solidly “overbought” territory, and that certainly warrants near-term caution but in no way demands that I sell positions. This will be a “Battle Royale” between the bullion banks, the algobots, and the East Asian buyers, who all have vested interests in maintaining the status quo.

I promise you that in the next week or so, the pundits will all have reasons for the breakout and/or profit-taking that will bounce the gold price around, but just remember that of all the expert commentators that will attempt to provide reasons for the breakout, there is only one entity that knows for sure why gold is moving in any one direction and that entity is gold itself.

Only gold truly knows. . .

The Dow Jones Industrials ETF

The Dow Jones Industrials ETF (DIA:US) has been stubbornly strong for the better part of five months and has weathered several possible storms that threatened to derail the move, but up until February 23, it looked unstoppable. This past week was another down week, but it was not only an orderly decline; there was zero consternation over anything, including a wonky jobs report, descending consumer confidence, and an obviously slowing economy.

I have been short the DIA through limited-risk and quite modest put positions for both December and March, and both have not entirely worked out as planned (a polite way of saying that they have been vaporized). However, when you hedge “small,” you are always able to fight another day, and that is exactly what I am doing with the June series of put options.

The U.S. stock market is ridiculously overvalued against the backdrop of a slowing economy, shrinking full-time job growth, and a looming debt bomb. However, the offset has been fiscal stimulus, which is the one tool that the Democrats believe can save the November election, where incumbent Joe Biden is sadly trailing. The inflationary tactics of the White House are the primary reason that I must keep by hedges “small,” and the reason lies in the following quote (which you have all read before): “Never underestimate the replacement power of equities within an inflationary spiral.”

It may just be that the stock market is telling us that we are in the early stages of a Weimar-style, Zimbabwe-esque hyperinflation that is “hiding in plain sight” with the 20% ascent since last October. In 1921-1923, in Germany, citizens were protected against the ravages of currency debasement and 100,000% inflation only through the ownership of equities, just as the top-performing market of the 1980s was the Zimbabwe Stock Exchange but only in terms of its domestic currency.

Uranium

On the topic of uranium, I sent out a chart last week of Cameco Corp. (CCO:TSX; CCJ:NYSE) when it was trading around $40 in which I called for a Fibonacci retracement move from under $40 to $44.14, which was also where the 100-dma and 50-dma converge.

The stock has since moved up to $44.47 on Friday and then proceeded to collapse to $41.23 on massive volume.

While I am still a believer in the uranium fundamentals, the bloom is definitely off the rose as the “U3O8 to $300!” has been muted by a checkback to under $100/lb., closing out the week at $93.50 for the high of $105 seen in February. I await CCJ:NYSE visiting the $39 level over the near-term action as an opportunity to replace the call options I and my subscribers sold when I put out the “SELL” at $51 on January 12.

As we proceed into the month of March and onward into 2024, the two metals to own are copper and gold, with positions in Freeport-McMoRan Inc. (FCX:NYSE), Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB), and Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB) comprising the bulk of the GGMA portfolio.

For now, though, gold reigns supreme.

| Want to be the first to know about interesting Gold, Critical Metals, Uranium and Base Metals investment ideas? Sign up to receive the FREE Streetwise Reports’ newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold Corp., Cameco Corp., and Norseman Silver / Fitzroy Minerals.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: All. My company has a financial relationship with Norseman Silver / Fitzroy Minerals. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.