tunart/E+ via Getty Images

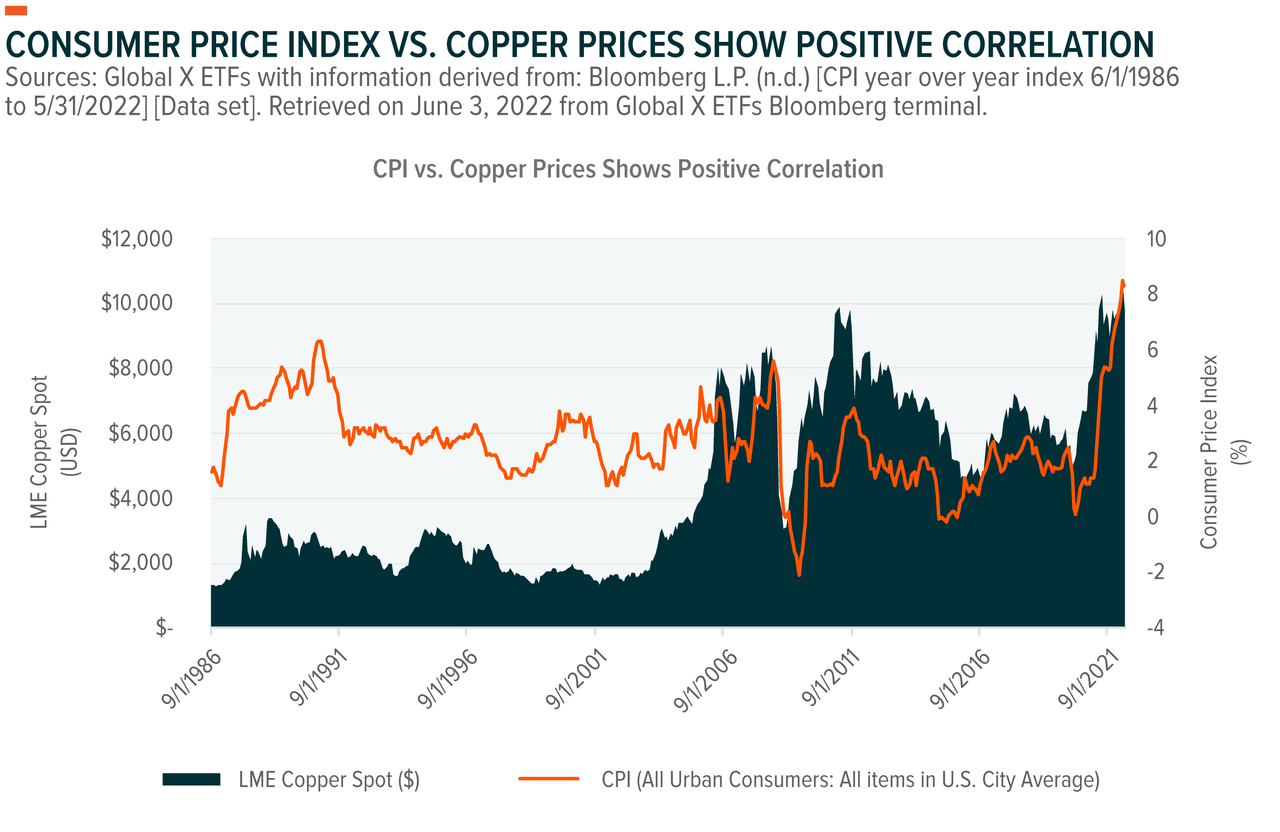

Historically when inflation rises, copper prices usually follow suit, and this cycle is proving to be no exception. The metal is one of the best-performing assets in the post-pandemic period thus far. Copper’s pervasive use throughout the global economy means that when activity picks up, copper demand tends to rise. The bullish case for copper today centers around sticky inflationary pressures, the lingering copper supply deficit, and economic activity slowly ramping up in the post-COVID period. Long-term, copper also offers many interests through its role in the global renewable energy movement, infrastructure spending, and climate policy targets from China. In this piece, we explore copper’s short- and long-term outlook and why investors may want to seek exposure to this base metal.

Key Takeaways

- Copper’s positive historical correlation with inflation can make it an attractive inflation hedge. In April, the Consumer Price Index increased by 8.3% annually, the fastest pace since January 1982.1

- Supply disruptions in Latin America could continue to drive up copper prices. Longer-term, copper’s critical role in decarbonization offers strong support for demand. Renewable energy capacity additions along with Electric Vehicles (EVs) could boost appetite for copper by 7.9% over the next 10 years.2

- Over the next decade, the balance between green and non-green demand for copper is expected to switch sharply, where green demand is expected go from 5% today to 16% at the end of 2030.3 China’s ambitious renewable energy spending plans are leading to these increased copper demand projections.

Copper Is an Economic Bellwether

Copper is widely viewed as a leading indicator of inflation and overall economic health. Every major sector of the global economy uses copper, from new home construction and factories to the automobile industry and power generation, amongst many others. The upstream nature of copper makes it easy for producers to pass rising prices through the supply chain to end consumers. As a result, copper prices tend to rise before general consumer prices rise. Many investors use inflation expectations to gauge when to buy copper, as it mirrors general economic growth trends.

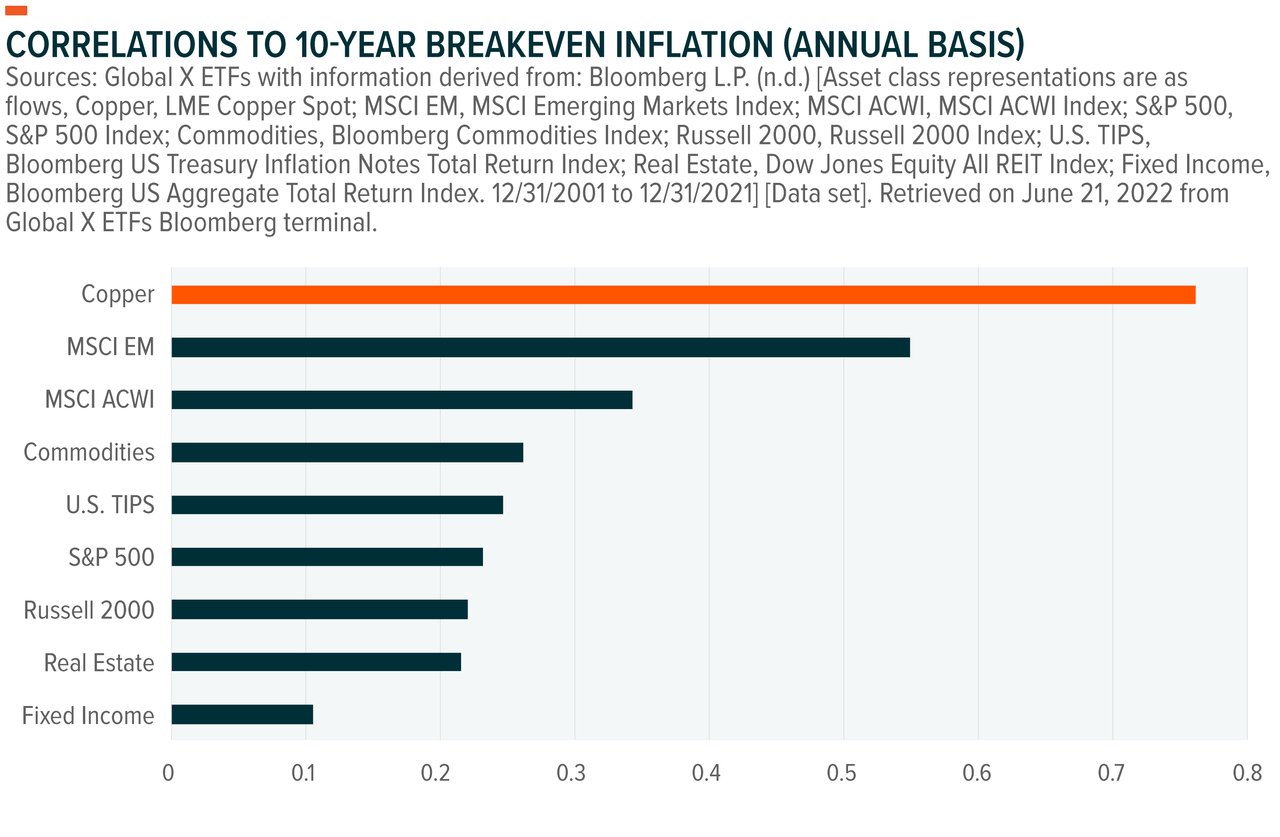

Copper also has the highest correlation with the 10-year breakeven inflation rate dating back to 2001. The heightened correlation among its peers is one of the many reasons that copper is traditionally one of the best-performing assets during inflationary periods.

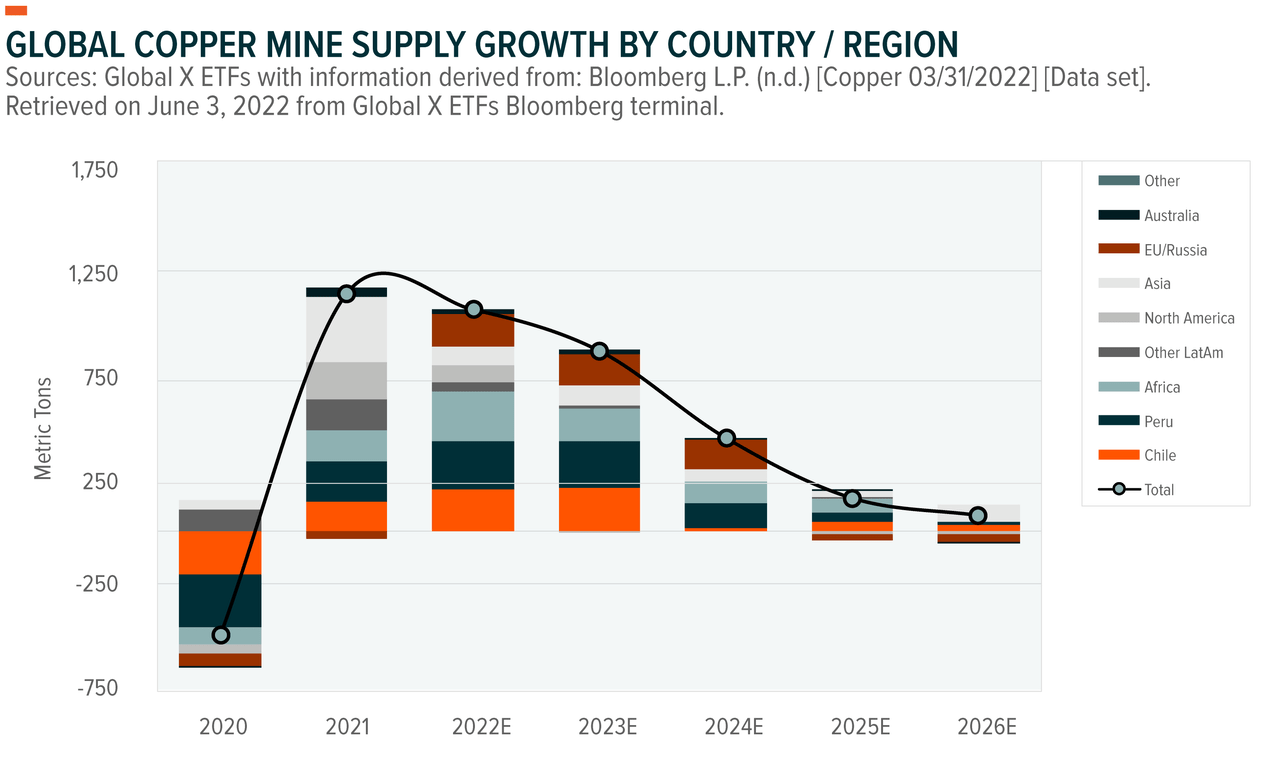

Ongoing Supply Deficit Could Support Higher Copper Prices

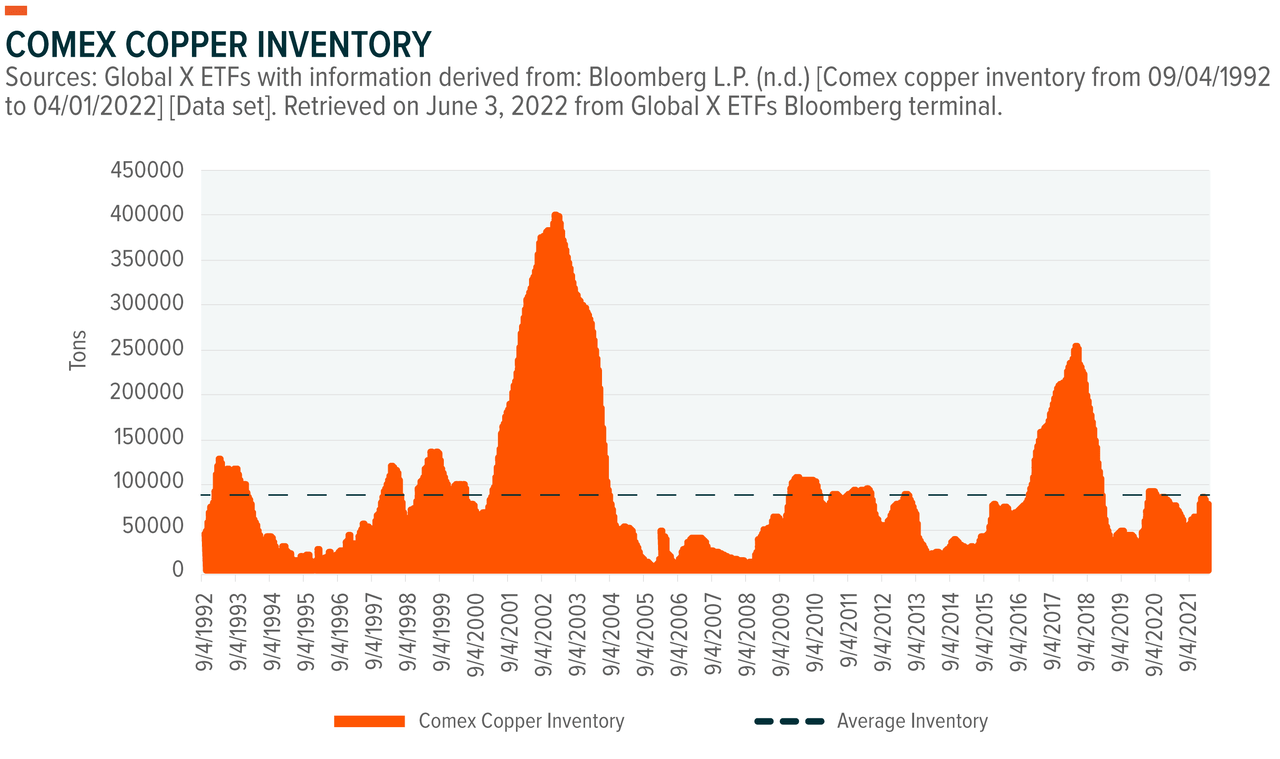

The copper supply deficit in 2022 is not expected to be as severe as it was last year, but even by 2030 a deficit is still expected to persist.4 The refined copper market had a deficit of 475,000mt in 2021, but forecasts are for supply to improve in 2022.5 Still, a handful of factors could help keep supply low and copper prices high, including low inventory levels in London Metal Exchange (LME) registered warehouses, accelerated decarbonization efforts coming from China, political risk in countries with higher copper production, inflation reaching 40-year highs, and slower production in Chile, a country that accounts for more than a quarter of the world’s copper supply.

In the near term, supply disruptions in Chile and Peru, which account for over 40% of global copper supply, are putting pressure on the global supply market. The Las Bambas mine in Peru, which supplies 2% of global copper, suspended operations in April after a protest from the local community. In Chile, March copper production fell 7.2% due to operational and water supply issues.6 Also, the longer-term outlook for Chilean supply may not be as strong with the new leftist political parties planning to implement a tax increase on the mines.7 The tax could curb the amount of new mining development sites and new copper supply growth.

Copper Is Core to the Green Energy Transition

When investors contemplate metals in the renewable energy transition, lithium, cobalt, aluminum, graphite and other rare earth metals may come to mind first. However, copper is considered one of the core material building blocks for the renewable power grid because it has the highest conductivity of all non-precious metals. This makes copper an ideal metal in the industrial electrical wiring used for electric vehicles and infrastructure projects as copper can carry more electrical current than other precious metals. Copper’s key characteristics—conductivity, ductility, efficiency, and recyclable—make copper omnipresent in renewables, from solar panels and EV batteries to thermal energy and wind turbines.

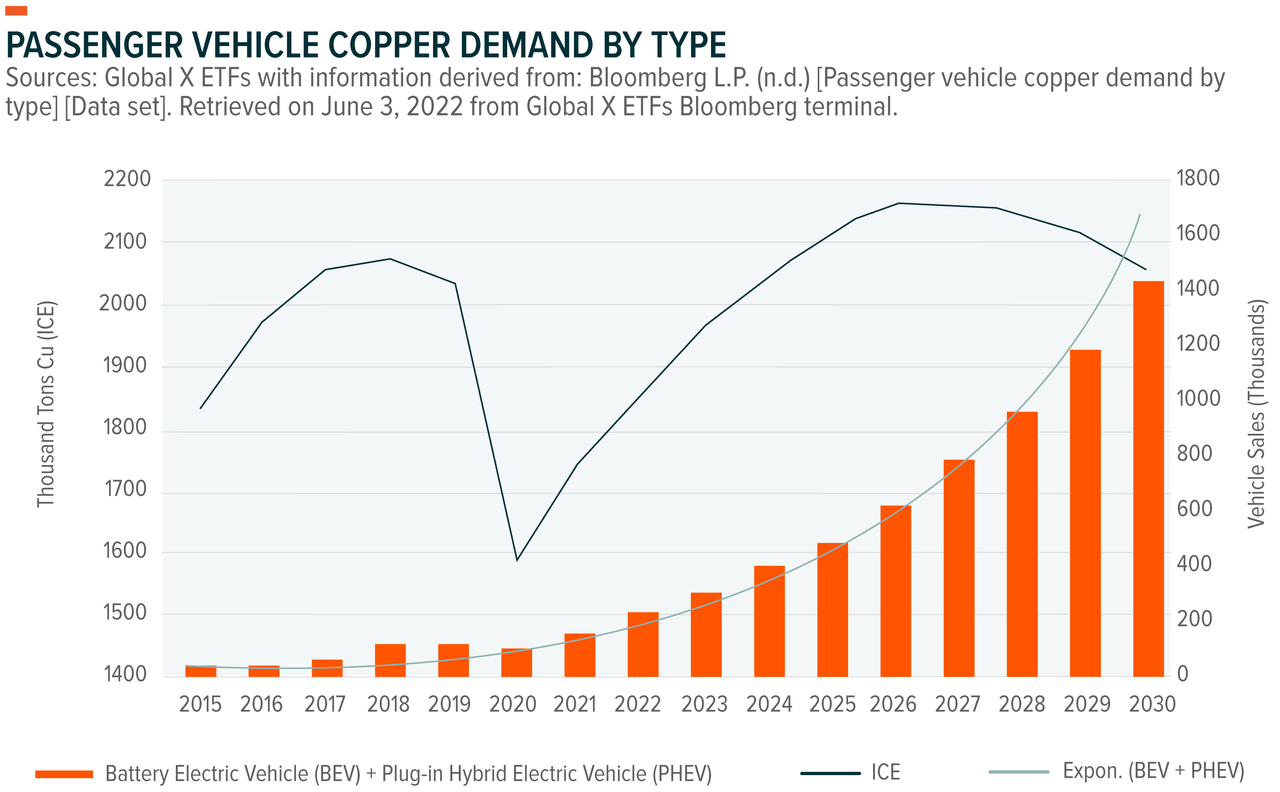

According to estimates, the EV sector alone would require more than 250% more copper by 2030 just for charging EVs, as EVs need nearly four times as much copper as internal combustion engine (ICE) vehicles.8 The global EV market, with more than 400% growth expected by 2029, is estimated to bring around 40% of copper demand by 2030.9 Annual copper demand for solar photovoltaic (PV) installation could more than double from 690,000 tons in 2020 to 1,500,000 tons by 2030, nearly triple by 2050, and grow to account for about 15% of copper production in 2025 as countries work toward achieving their net-zero emissions goals.10

We spoke in our March 2021 copper report that China’s “new infrastructure” plan and President Biden’s plan to push clean tech and upgrade America’s infrastructure accelerated copper’s demand. Biden signed the $1 trillion infrastructure bill into law last year, allowing the government to spend over $7.5 billion over five years to help build a network of EV charging stations throughout the country.11 Infrastructure spending is key for copper’s demand and by 2025, green demand is expected to double, going closer to 3 million tons.12

China’s Copper Demand Expected to Outweigh Short Term Challenges

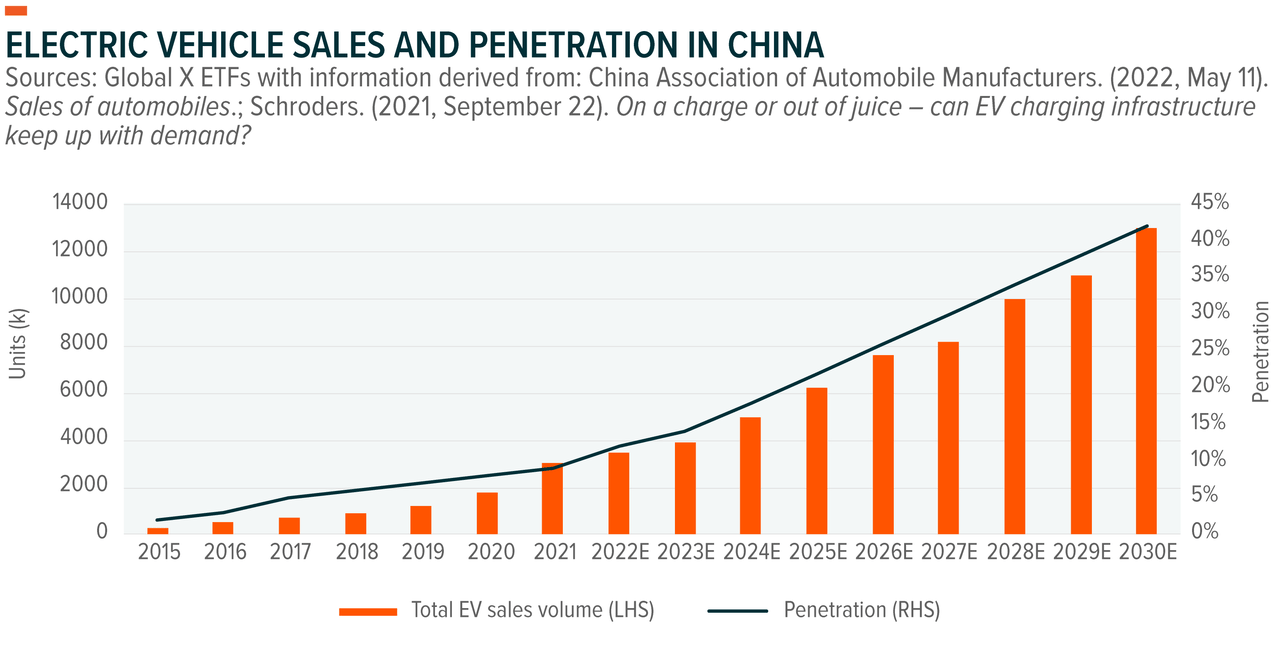

Copper demand may face headwinds in China currently with the fluid situation of lockdown measures, but a quick rebound in consumer goods and improved infrastructure demand can lift Chinese copper demand above 2% for 2022.13 China is the world’s biggest copper market, consuming approximately half of all global output. Longer-term, China’s renewable energy plans are expected to boost copper demand. Beijing aims to bring total wind and solar capacity to 1,200 gigawatts by the end of 2030, almost doubling the current level.14 The government also wants to build a $300 billion clean grid, connecting green power to rural areas and mega cities. This mega project requires thousands of kilometers of ultra-high voltage power lines, and copper’s high conductivity and tensile strength make it the metal of choice. Also, a good portion of growth comes from the Chinese EV market, where the country sold over 3 million units in 2021, compared to the U.S. at around 600,000 units.15 As the Chinese EV market is growing rapidly around large cities, EVs in China are expected to account for over 40% of new vehicle sales by 2030 and 60% by 2035.16 The infrastructure and auto segments together account for 55% of China’s copper needs. 17 Copper demand will be impacted by growing the market size of EVs over the next decade, especially in China where the government is pushing for a green transition by 2030.

Conclusion: Copper Prices Can Stay Higher, for Longer

2022 is proving to be a volatile year, with inflation hitting multi-decade highs as the real economy still recovers from the pandemic, global monetary policies turn hawkish, and the effects of Russia’s invasion of Ukraine spreads across the economy. However, base metals like copper have done well in inflationary environments like these, given the metal’s high correlation with inflation, the role it plays in the traditional economy, and the one it’s set to play in the green economy. We believe that with the shift towards carbon neutrality, the acceleration of EV penetration, and the massive infrastructure investment to meet climate change goals, copper demand can persist over the long term.

FOOTNOTES

1. Bureau of Labor Statistics. (2022, June 10). Consumer price index – May 2022 [Press release]. U.S. Department of Labor. https://www.bls.gov/news.release/pdf/cpi.pdf

2. Mining.com Editor. (2021, June 28). Energy: Green copper demand to average 13% annual growth over next 10 years – report. Mining.com. Green copper demand to average 13% annual growth over next 10 years – report – MINING.COM

3. Kaya, N. E. (2021, May 3). Green transition could boost record high copper demand. Anadolu Agency. Green transition could boost record high copper demand

4. Holman, J. (2022, May 11). S&P Global Commodity Insights: Massive copper supply required for electrification of global economy: Friedland. S&P Global Inc. Massive copper supply required for electrification of global economy: Friedland

5. International Copper Study Group. (2022, April 22). Copper: Preliminary data for January 2022 [Press release]. Retrieved from Press Releases

6. Cambero, F., & Villegas, A. (2022, April 29). Chile’s March copper production falls 7.2%, manufacturing output up 3.3%. Mining.com. Chile’s March copper production falls 7.2%, manufacturing output up 3.3% – MINING.COM

7. National Minerals Information Center. (n.d.). Copper statistics and information. U.S. Department of the Interior (USGS). Accessed on June 13, 2022 from Copper Statistics and Information

8. Jamasmie, C. (2019, August 12). EV sector will need 250% more copper by 2030 just for charging stations. Mining.com. EV sector will need 250% more copper by 2030 just for charging stations – MINING.COM

9. Erkul, N. (2021, May 3). Renewable, World: Green transition could boost record high copper demand. Anadolu Agency. Green transition could boost record high copper demand

10. IRENA. (2019). Future of Solar Photovoltaic: Deployment, investment, technology, grid integration and socio-economic aspects (A Global Energy Transformation: paper). International Renewable Energy Agency, Abu Dhabi. https://irena.org/-/media/Files/IRENA/Agency/Publication/2019/Nov/IRENA_Future_of_Solar_PV_2019.pdf

11. The White House. (n.d.). President Biden’s bipartisan infrastructure law. Accessed on June 13, 2022 from President Biden’s Bipartisan Infrastructure Law | The White House

12. Mining.com Editor. (2021, June 28). Energy: Green copper demand to average 13% annual growth over next 10 years – report. Mining.com. Green copper demand to average 13% annual growth over next 10 years – report – MINING.COM

13. Barrera, P. (2022, April 25). Copper investing: Copper price update: Q1 2022 in review. Investing News. Copper Price Update: Q1 2022 in Review

14. Ng, E. (2022, January 27). Business, climate change: China’s new wind and solar capacity makes up over half the power industry total as nation seeks to cut carbon footprint. South China Morning Post Publishers Ltd. Wind and solar make up more than half China’s added power capacity

15. Marquis, C. (2022, March 11). Business & Technology: The state of China’s electric vehicle market with Robert Yu. SupChina. The state of China’s electric vehicle market with Robert Yu – SupChina

16. Automotive News. (2019, September 8). China: China explores ambitious goal for EV sales by 2035. China explores ambitious goal for EV sales by 2035

17. Reuters. (2021, October 7). Copper analysts reset outlook on China’s dual demand ructions. Copper analysts reset outlook on China’s dual demand ructions

GLOSSARY

Correlation: Correlation is a measure that shows how two securities move in relation to each other. A correlation of 1 implies that the securities will exhibit the same price movements. A correlation of 0 means the securities demonstrate completely unrelated price movements.

COMEX (The Commodity Exchange): Primary futures and options market for trading metals such as copper, silver, gold and aluminum.

Bloomberg US Aggregate Total Return Index: The Bloomberg US Aggregate Total Return Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, Mortgage-Backed Securities (agency fixed-rate pass-throughs), Agency-Backed Securities and Commercial Mortgage-Backed Securities (agency and non-agency).

Dow Jones US Equity All REIT Index: The Index is designed to measure all publicly traded real estate investment trusts in the Dow Jones U.S. stock universe classified as equity REITs according to the S&P Dow Jones Indices REIT Industry Classification Hierarchy. These companies are REITs that primarily own and operate income-producing real estate.

Russell 2000: A small-cap stock market index that includes 2,000 smaller companies that focus on the U.S. market.

S&P 500: S&P 500 Index tracks the performance of 500 leading U.S. stocks and captures approximately 80% coverage of available U.S. market capitalization. It is widely regarded as the best single gauge of large-cap U.S. equities.

Bloomberg US Treasury Inflation Notes Total Return Index: Measures the performance of the US Treasury Inflation Protected Securities (TIPS) market.

Bloomberg Commodity Index: Bloomberg Commodity Index is calculated on an excess return basis and reflects commodity futures price movements.

MSCI ACWI Index: MSCI ACWI Index captures large and mid-cap representation across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries. The index covers approximately 85% of the global investable equity opportunity set. DM countries include: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the UK and the US. EM countries include Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Russia, Qatar, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates.

MSCI Emerging Markets Index: A flagship hard currency Emerging Markets debt benchmark that includes fixed and floating-rate USD dollar-denominated debt issued from sovereign, quasi-sovereign, and corporate EM issuers

London Metal Exchange (LME) Copper Spot: Copper price from the end of London Metal Exchange final day evening evaluations.

Investing involves risk, including the possible loss of principal. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles, or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments may be subject to higher volatility. There are additional risks associated with investing in copper and the copper mining industry. COPX is non-diversified.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns.

Carefully consider the fund’s investment objectives, risks, and charges and expenses. This and other information can be found in the fund’s full or summary prospectuses, which may be obtained at globalxetfs.com. Please read the prospectus carefully before investing.

Global X Management Company LLC serves as an advisor to Global X Funds. The Funds are distributed by SEI Investments Distribution Co. (SIDCO), which is not affiliated with Global X Management Company LLC or Mirae Asset Global Investments. Global X Funds are not sponsored, endorsed, issued, sold or promoted by Solactive AG, nor does Solactive AG make any representations regarding the advisability of investing in the Global X Funds. Neither SIDCO, Global X nor Mirae Asset Global Investments are affiliated with Solactive AG.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.